Inflation is here. You must protect your life savings.

Posted by John T. Reed on

• Home prices are soaring.

• Car prices and rental rates are soaring.

• Gold and silver prices are soaring.

• Oil and gas prices are soaring.

• Groceries are soaring.

• Lumber prices are soaring.

• Paper prices are soaring.

• In April 2021, the consumer price index went up at an annual rate of 11%.

• The year-over-year increase for the 12 months ending in April 2021 was 4.2%, the highest in 13 years.

.

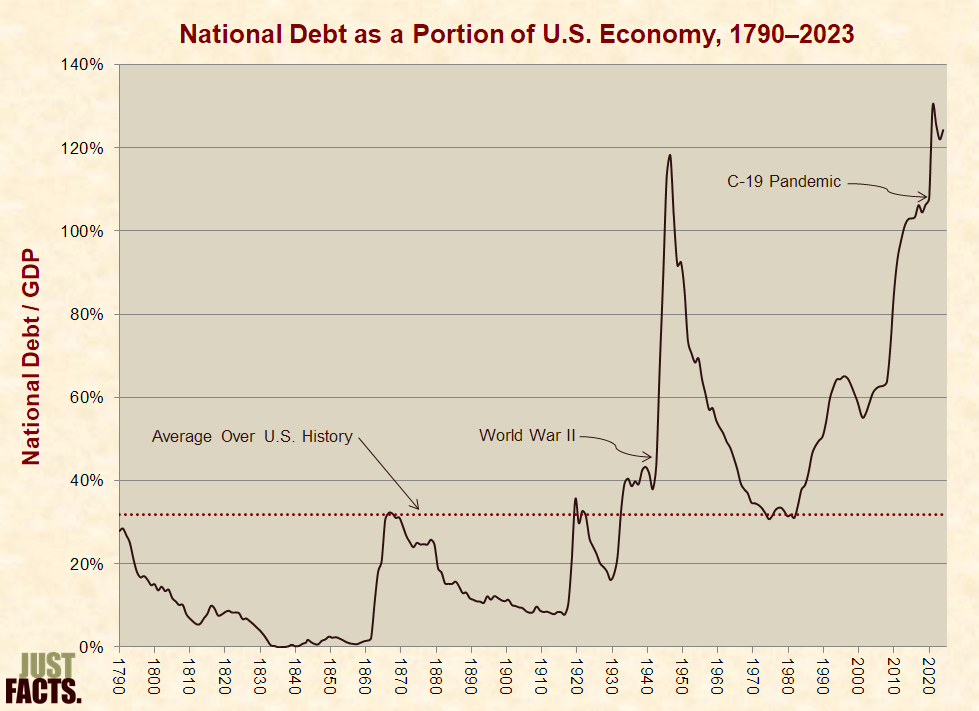

Here is a great graph that shows the problem that the politicians and their media allies are trying to say this graph has no significance.

.

https://www.justfacts.com/images/nationaldebt/debt_gdp-full.png?fbclid=IwAR0SZ9ZXToyyLIAf0KqRtQ08FfmtkaTft9AI3r7BQiF_rAdapTqaL-Ge-_w

{kind=link}

I warned readers over the last 11 years that hyperinflation could hit without warning. But it looks like we ARE getting warning, in the form of all the high inflation currently besetting us. That can help you if you still have not arranged your assets and liabilities to minimize damage from inflation and to take advantage of the opportunity to profit from debts you owe falling in real (adjusted for inflation) value. But if you ignore the warning we are fortunately getting, you will suffer avoidable losses.

My book How to Protect Your Life Savings From Hyperinflation & Depression applies to regular inflation and double-digit inflation as well.

I lived through double-digit inflation in the 1970s and 1980s. Most of the same advice applies to both double-digit inflation and hyperinflation:

- owing fixed-rate debt is good

- owning fixed-rate debt is bad

- fixed annuities like social security and pensions are bad

- dollar-denominated assets are bad (Which are those? Any asset with a dollar sign on your proof of ownership. The one many people get wrong is stocks. Those are NOT dollar-denominated. Look at your stock certificate. No dollar sign. Stock ownership is denominated in the number of shares you own. A bond, in contrast, has a dollar sign.)

- non-dollar denominated assets are good—What are they? commodities, real estate, forever stamps, the melt value of coins (coinflation.com), foreign currencies (you must hold them outside of the US), business inventory

- indexes Work for low inflation, but the faster the inflation, the more indexation is a cruel joke.

- buying everything you need for the rest of your life is hard, impossible, but you need to try to do it as best you can

- Barter is almost certain in high inflation, but you almost certainly have only a tiny number of barterable things—buy far more. My book lists the characteristics of good barter items.

- Are stocks good hedges against inflation? No. they tend to go up, down, and sideways in high inflation. It depends in part of how much of the advice in my book the corporation has wittingly or unwittingly followed.

- You need to stay liquid enough to pay routine bills. You can’t eat real estate or gold. But there are many relatively liquid, non-dollar-denominated assets.

My book How to Protect Your Life Savings From Hyperinflation & Depression cover all this and more.

It appears that you still have time to follow much of its advice. But it also appears that hedges against inflation are being taken away one-by-one in recent months. So you’d better use the fewer opportunities that remain before they, too, are eliminated.

Share this post

0 comment